When I logged into my brokerage account today, I was pleasantly surprised to see my Canadian index fund popping 1% on strong bank earnings. The banks make up one third of the Canadian index, so when they do well, Canadian index fund holders tend to do well. But the bigger news here is that the banks are raising their dividends, yet again.

TD is raising its quarterly dividend from $1.05 to $1.08 per share

BMO is raising its quarterly dividend from $1.63 to $1.67 per share

CIBC is raising its quarterly dividend from $0.97 to $1.07 per share

What exactly is a dividend and how can it help us build wealth? Basically, when a company makes a profit, it can either invest that money back into the business, or it can return the money to shareholders in the form of a dividend. Dividends are a way for companies to both reward their shareholders and entice them to buy even more shares.

If a company pays a dividend, the share price will have a ‘yield’, which shows investors how much they can expect to receive in dividend income. For example, if a company’s share price is $100 and it has a current yield of 2%, then investors can expect to receive around $2 annually, or 0.50 cents every quarter.

Free money – sounds pretty sweet, right? Well, we need to remember that a dividend isn’t exactly free money. It’s money that the company is actively choosing not to invest back in the business, which means that theoretically, the company will be less profitable than it could have been, had it reinvested the dividend in something that would drive growth and profits, like AI infrastructure or faster shipping.

That’s why it’s important that as investors we focus on index funds that offer overall growth potential and not just be tempted to buy individual stocks or index funds for the high dividend yield alone. This is known as ‘yield-chasing’, and a lot of investors tend to fall into this trap, sacrificing growth for steady income. They’ll invest a million dollars into a company offering an 8% yield and pat themselves on the back for being so smart for locking in 80k/year for life, not realizing that their million-dollar capital is steadily eroding. Pfizer is an example of a company that pays an attractive dividend of 6.7%, but is down 18% over the last decade! It’s also important to remember that companies can cut their dividends in a downturn, as we will see below when we look at what happened during the Global Financial Crisis of 2008-09.

But you and I aren’t chasing yield, and we don’t hold individual stocks. We are passive index fund investors who own the entire market through an index funds like Vanguard All-Equity ETF Portfolio (VEQT), which is comprised of thousands of Canadian, US and International companies focused on growth, with some companies paying a small, consistent dividend. Let’s look at the dividend yield in the Canadian index specifically, using the Vanguard FTSE Canada All Cap Index ETF (VCN).

From VCN’s fund prospectus or even by Googling its stock chart, we can see that VCN is trading at $64.26 per share and paying out an annual dividend of $1.47. We can calculate the yield by dividing the annual dividend by the current share price:

$1.47 divided by $64.26 = a yield of 2.28%

To put this in context, if we were to invest $1 million CAD today in VCN, we would essentially be locking in around $22,800/year in annual dividend payments.

Now here’s where things get interesting…

Back in 2015 VCN was trading much lower – around $30 per share, and paying an annual dividend of 70 cents per share, which resulted in a yield of 2.3%, similar to today’s yield of 2.28%. Along came Snowball, our early-retiree piggy bank. He saved up $1 million dollars and decided to invest it all in VCN and live off the 2.3% yield. At $30/share he was able to buy 33,333 shares of VCN, which gave him an annual dividend payment of $23k (70 cents annual dividend per share x 33,333 shares = $23,333)

23k/year would have been a healthy amount of dividend income for Snowball to retire on in 2015. More than enough to escape to Thailand during the harsh Canadian winters! Now suppose Snowball had decided to do just that and live off the $23k/year in dividend income while letting his original million-dollar investment in VCN grow over time. Thanks to the Toronto Stock Exchange’s strong performance over the last 11 years, that million dollars would be a whopping $2,141,978 today! Snowball would be one wealthy, well-tanned piggy bank!

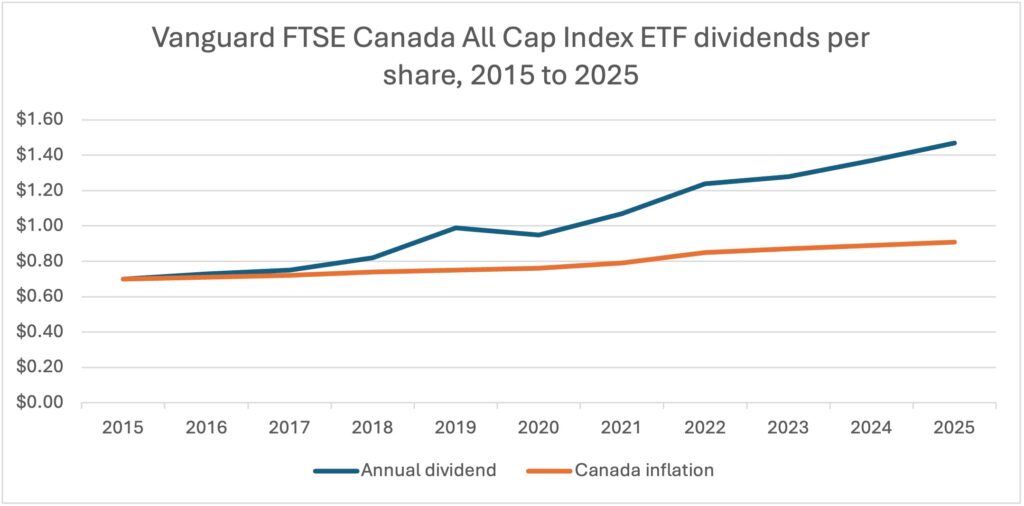

But an even more interesting trend emerges when we look at an 11-year chart of VCN, and it has to do with those annual dividend payments…

The dividend payments have risen with time, year after year, even out-pacing inflation!

Source: https://dividendhistory.org/payout/tsx/VCN/ and Bank of Canada Inflation calculator

While VCN has gone up in value from $30 to $64.26 per share, the dividends have also increased from 70 cents to $1.47 annually!

Even if Snowball had spent every penny of his annual dividend payment relaxing on the beaches of Koh Phi Phi, as long as he held onto his 33,333 shares, by 2025 his annual dividend payment would be:

$1.47 annual dividend payment per share x 33,333 shares = $49k!

That’s more than double the dividends he signed up for back in 2015, because many of the dividend-paying companies in the Canadian index have been steadily raising their dividends over the years just like the banks did this morning! An early retiree like Snowball who bought $1 million of VCN in 2015 would have grown both capital and annual dividend payments, outpacing inflation by a long shot. And the Canada Dividend Tax Credit would have made the annual dividend payments tax efficient, ensuring Snowball paid as little income tax as possible while he baked in the sun. I’ve never been more jealous of a fictional piggy bank.

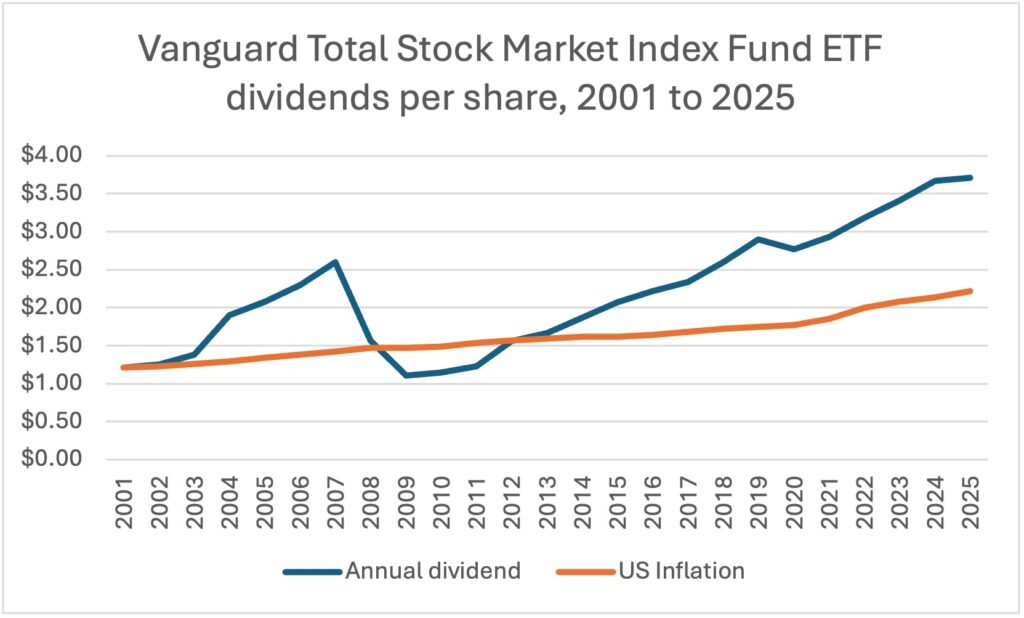

And it’s not just the Canadian companies that increased their dividends over time. We have 25 years of data for the Vanguard Total Stock Market Index Fund (VTI) which tracks the Total US stock market. Despite some volatility during the Global Financial Crisis, the dividends in the Total US stock market have also gone up with time.

Source: https://dividendhistory.org/payout/VTI/ and US Inflation calculator

If we zoom in on 2008-11 we can see that not only did many US companies cut their dividends during the Global Financial Crisis, but inflation actually outpaced the annual dividend payments during those cold, bleak years. Anyone relying on dividends as their sole source of income would have been in a pickle. There really is no safe haven in a major market crash which is why it’s always a good idea to have a few years’ worth of cash on hand and remember that we are investing for the long term.

But the key here is that the Global Financial Crisis was a temporary event, as were the cuts to dividends. US dividend payments rebounded along with stock prices just a few years later. By 2012 the Total US stock market’s annual dividend payments were back to their inflation-adjusted baseline and continued growing in an upward trajectory for the next 13 years. Additionally, during 2008-09 stocks were 30-50% off. Anyone who re-invested their dividends through a Dividend Reinvestment Plan (DRIP) would have picked up even more shares at rock-bottom prices, further contributing to portfolio growth and higher dividends over the years.

Whether you are still in your wealth accumulation stage or sizzling away somewhere hot and tropical like Snowball, dividends can help you build wealth through the ups and downs of the stock market. If you’re still building your nest-egg and have a DRIP set up, you can rest easy through market drops knowing your dividends will be re-invested on a regular basis, picking up more shares at a discount. And for early retirees, dividends can be a great steady source of income to look forward to, provided you have a back-up plan to help you weather the storm in the event of a global financial melt-down. While past results don’t dictate future results, being able to visualize steadily rising dividend payments over the years is motivation enough for me to pick up a few more shares of VEQT and – as always, stay the course.

Do you get excited about dividend payments? Do you have a Dividend Reinvestment Plan (DRIP) set up? Let’s hear it in the comments!

Disclaimer: I am not a financial advisor. None of this is financial advice. I encourage you to do your own research.

Leave a Reply