By August, after the military movers loaded our belongings onto a truck and we drove four hours to start our new life, the stock market had fully recovered its 30% loss and was marching higher. Ever since the stock market had bottomed just four and a half months earlier, I had continued to invest vigorously with every paycheck, only making a one-time withdrawal from my RRSP to cover part of the down payment on our new home. As a result, my portfolio was now in the green and larger than ever as I had continued purchasing index funds at fire-sale discounts.

So much had changed in those four and a half months. Covid was still spreading through the world like wildfire, and many were mandated to work from home. As our government had asked us to stay in social bubbles of 10 people or less, there were no summer weddings or backyard BBQs commonly found in a typical summer. Nor was there any travel as most international flights had been cancelled, the wide skies overhead a silent blue. Instead, people began to explore their own backyards, some heading up north to rent a cottage or an RV. So when we rolled up to the Hilton Homewood Suites along the shores of Lake Nipissing where we would be staying for a month, I was not surprised to see a myriad of families enjoying the large sandy beach. As I tend to gravitate to any sparkling body of water in my vicinity, I grabbed Victor and we jogged down the hill to check out the picturesque waterfront.

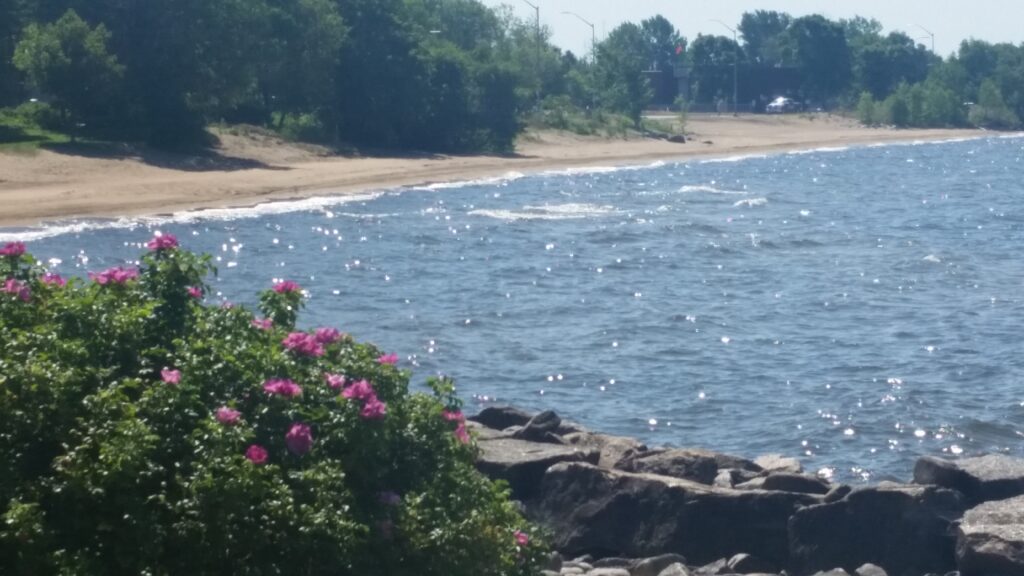

Lake Nippissing was a large freshwater lake bordered by North Bay’s signature pine trees in the hilly distance. Boisterous children ran through the clear shallow water, squealing with delight as they kicked up their heels to splash their parents. Others stayed on land building sandcastles in the warm August sun while their caregivers scrolled Facebook on their iPhones. In these isolating times people yearned for connection and entertainment, and technology was there to assist. As a result, the mega-cap technology stocks known as the FAANG stocks (later becoming the Magnificent 7) were surging. Technology companies like Facebook (Meta), Apple, Amazon, Netflix and Google exploded during the Covid pandemic, making many investors wealthy. As an index investor, I was grateful that I was invested in the Total US stock market as one third of the index was comprised of technology companies yielding big returns for any investor holding US broad-based equities.

Across the lake a large stretch of trees on Manitou Island lined the horizon. To our left a wooden pier stretched out into the water, its creaky wooden beams supporting an ice cream shop and hot dog stand. A paved promenade snaked down the hill, surrounded by inukshuks and pink flowers, currently being pollinated by a swarm of bumble bees. There was even a waterside patio that served pints of local beer and fish & chips. With no planes in the air the waterfront was a hazy mid-afternoon quiet. The sun bounced off the water and the trees were emerald, green from all the rain that had fallen earlier that summer.

As I breathed in the clean air, a mix of pine, muddy freshwater lakes, deep fried foods and coconut-scented sunscreen, I could not believe my luck. Just six months earlier I had been stuck in a snowy subway delay on my way to a grueling week-long workshop. Now I was spending a month in a comfortable hotel along the water, my schedule more flexible than ever, my investments working overtime. I would have time every morning to jog along the promenade, to slow down and spend time outside. Most importantly, I got to continue living with my husband full-time, in one of the most beautiful places I had ever seen.

At the same time, people all around the world were suffering from the now out-of-control pandemic. Many had died, others were fighting for their lives, while still more had lost their jobs or their businesses. I was grateful for my own good fortune, but I also felt extremely guilty that Covid-19 seemed to have benefited me while robbing others.

“It’s out of your control,” Victor assured me when I explained my feelings to him. “We just need to make sure we don’t spread the virus, and to be thankful for everything we have.”

I slipped off my sandals. The sand was warm and grainy beneath my feet. I took a bite of my raspberry ripple ice cream and tasted the creamy sweetness. I closed my eyes and felt the warm sun caress my skin, heard the waves lapping against the shore. Victor was right. I had so much to be grateful for.

The days I spent living in a 3-star hotel on Lake Nipissing were some of the happiest of my life. With most of my stuff in storage I was forced to live like a backpacker – and I loved every minute.

Every morning I would wake up to the sun streaming through the fly-encrusted hotel window. “It’s a beautiful day in the Bay!” I would exclaim as I sipped my instant coffee and looked out across the parking lot of RVs and out towards the lake.

I jogged along the water’s edge, stopping to admire the bumblebees hovering over the lavender and watch the rippling waves. I still had online meetings to attend but most days I could log off late-afternoon and find a shaded spot on the beach. The sky was clear. Light shone through the trees, dappling the sand. I floated in the shallow water, listening to children splash their exasperated parents. Later I would return to our room, my skin warmed by the sun, my body swimming in a vitamin D-infused euphoria.

I had always thought it would be difficult to leave the big city behind. I had worried about it back in Winnipeg, when I first learned to invest. But now all the things I had once been attached to were gone. All the trendy restaurants were closed. Friends had moved out of the city for greener pastures. Now, I found myself drawn to the simple, free things in life. Waking up to the sun, moving my body, spending time outside, watching the sun set along Lake Nippissing with Victor at the end of the day. For me, this was the good life. It wasn’t yachts and mansions and first-class flights abroad. And it certainly wasn’t promotions and accolades. What was the point of spending your life climbing the corporate ladder when an unpredictable virus could knock you over any minute?

During my relaxing afternoons on the beach, I read JL Collins’ A Simple Path to Wealth. In his book and on his blog JLCollinsnh.com, Collins explains the stock market in a clear, digestible way. He also introduces beginner investors to the concept of financial independence. He suggests that if you are invested in a broad-based low-cost index fund such as VTSAX which tracks the US Total Stock Market, once you can live off of 4 percent of your portfolio, “you are financially free.” (source). At this point you no longer need to work if you don’t want to, because your portfolio funds your lifestyle.

I pictured having a portfolio so large that 4 percent could power my whole life. I could only imagine the freedom. At this point I still wasn’t sure how long my office would be closed, how long I could live this dream-come-true up north with Victor. While I didn’t want Covid to hurt anyone, I would be lying if I said I wasn’t benefitting greatly from the way in which the world had changed so suddenly. While I was not yet financially independent, my globally diversified low-cost portfolio had allowed me to begin this new life. It was showing me what my future could be like if I kept growing my wealth. But my office could call me back any minute, and it would be back to the harsh lighting and windowless rooms, and away from Victor and the fresh northern air.

But maybe, just maybe, if I kept growing my portfolio, I could withdraw 4 percent per year and my dreams could come true every day.

“The less you need, the more you are free,” JL Collins whispered in his soothing voice as the wind rustled the pages (source).

I thought about all my things in storage, the clothes I had stopped buying. Over the years I had whittled away the need for material things, and now I was getting a glimpse into what could be a peaceful, free future if I continued to reduce my needs and embrace minimalism. The less money I spent on things, the more I could invest, and the faster I could live a peaceful life on my terms. As I scrolled through my budgeting app I noticed that my annual budget had indeed gotten smaller over the years. Still, 4 percent of my portfolio could not yet cover my annual expenses. But one day it might.

The afternoon sun began to set, signaling time’s relentless march. I was not going to quit now.

Repeatable steps I took that you can too!

- Check in with yourself throughout your wealth-building journey. Are you still the same person that you were when you started? Have your values changed? Has the world changed? What would you spend your days doing if you didn’t have to work for a living?

- Add up your monthly budget and multiply it by 12 to get your annual budget. Is it 40k? 50k? 100k? If you multiply that by 25, you’ll get an idea of how much you would need to become financially independent and live off your portfolio indefinitely. For example, if your annual budget is 40k and you multiply that by 25, you would need a million-dollar portfolio to safely withdraw 4 percent, or 40k a year. We’ll get into risk and safe withdrawal numbers in Chapter 13, but this exercise gives you a good idea of what you might be working towards.

- Is your annual budget too high for financial independence? If so, are there any areas you can cut to bring your annual budget down? The smaller your annual budget, the smaller a portfolio you will need to become financially independent.

- Have recent events such as a recession caused more risk to your portfolio?

Disclaimer: I am not a financial advisor. None of this is financial advice. I encourage you to do your own research.

Leave a Reply