Disclaimer: I am not a financial advisor. None of this is financial advice. I encourage you to do your own research.

2015 was the year of the app. There was an app to log your calories, measure your sleep, and yes, keep a budget. Even as an Android user the options were endless. I chose the best free app at the time, Moneywise Pro. I logged all my expenses on the app, forecasting months in advance. I included my income and fixed expenses such as my 2k/month savings, rent, utilities, cable, gym pass and yoga studio. Once I saw how little money I had leftover to pay for groceries, dinners out with friends, spa days and take-out, I decided to do some cost-cutting. I cancelled my cable and monthly memberships to my gym and yoga studio, opting to run outside for free and do yoga in my apartment. I kept my monthly dinner dates with my best friend since catching up over tacos in a cozy candle-lit bar helped us both get through the long dark winter. I tried to cut the things I could live without and kept what was important to me.

“Are you sure you want to give up your yoga membership?” my Dad asked, concerned, during Sunday dinner.

“Dad, I simply cannot afford it. I’m on a budget now,” I said proudly.

“But you love yoga!” He protested. Maybe he was right. Was I giving up too much? While I was steadily working towards a future of financial freedom, my one life was here and now. Millennials loved using the term YOLO (You Only Live Once). What if died tomorrow? Would I wish that I had spent more money on the present moment enjoying myself? Or, would 40-year old me wished that I had saved even more? I wrestled with this question for everything I gave up, and hoped like heck that I would still be alive in my 40s to enjoy the large portfolio I was growing.

While I worked through my budget and corresponding existential crisis, I still had an actual job to go to. On the subway I started playing around with an app called Loan Calculator that calculated compound interest. Compound interest is what Albert Einstein called “the eighth wonder of the world,” and it is what makes index investors wealthy over time. It means that the interest you earn on your original investment goes on to make its own interest. Then that interest goes on to make its own interest. Meanwhile your original investment is still making more interest… all of your interest gets compounded together until it’s one giant green arrow rocketing towards the sky!

I already knew from reading Millionaire Teacher that the stock market has returned an average of 10 percent per year over the last hundred years (source). But because I was on a time crunch to build my nest egg by my 40s I thought it better to forecast more modest future returns which would force me to save more. I settled on an annual return of 6 percent per year, which would allow for an 8 percent real return, 2 percent of which would be attributed to future inflation.

“Let’s see,” I would think to myself. “I have 100k now, and I’m saving $2,000 per month. If the market returns 6 percent every year for the next five years, that’s…$273,509!” My eyes widened at the thought of becoming a quarter-millionaire in just five years. “Now what if I bring my lunch to work, only buy ONE nice outfit for the office and stop getting manicures, saving me another $250/month? That would grow to almost $300,000!” I almost spit out my latte. “What if I stopped buying lattes…” I quickly became addicted to this game and started to ruthlessly cut every frivolous expense I could find. For me the act of budgeting and plugging those potential savings into a compound interest calculator worked hand in hand. Once I saw the future compounded returns of something I had budgeted for, I could evaluate it and decide if it made more sense to enjoy the luxury now, or forego the short-term pleasure, invest the money and reap the benefits in the future.

While I’m not suggesting you give up every little thing that makes you happy, after running the numbers myself I think it’s at least worth doing this exercise to see how much your daily expenditures are truly costing you in the long run. Then you can run your own “cost/benefit analysis” to decide if you want to keep the item or invest the money instead. In other words, is the short-term pleasure worth the opportunity cost that the invested money could make if invested longer-term in the stock market? And not every expense makes us happy, like the extra money we might be spending on bank fees and credit card interest. Could that money be redirected into the stock market? Could you switch internet providers and get the same service but for cheaper, freeing up capital for your long-term financial freedom?

Before you run the numbers, let me first tell you about my life-long coffee addiction that cost me over a quarter million dollars in stock market returns.

One of my earliest memories is of my Mom enjoying a cup of coffee in the living room. I was an energetic two-year-old and she needed her caffeine fix! I was curious as to what she was drinking and pawed at her for a taste. Exhausted, she dipped her finger into her mug and let me try a tiny taste of the creamy, sweet goodness. Surely a two-year-old would be turned off by the smokey bitterness that only adults appreciate. But I was hooked. By the time I was in grade five I was brewing myself a pot of coffee every morning before softball practice. Three years later Starbucks opened their first stores in Canada, one conveniently placed at the top of my street. I started knocking back frappucinos on my morning subway rides to middle school. By 16 I was working for the caffeine giant, inhaling double-espresso shots during long shifts. And today I’m still hooked, no morning complete without my morning Nespresso pod.

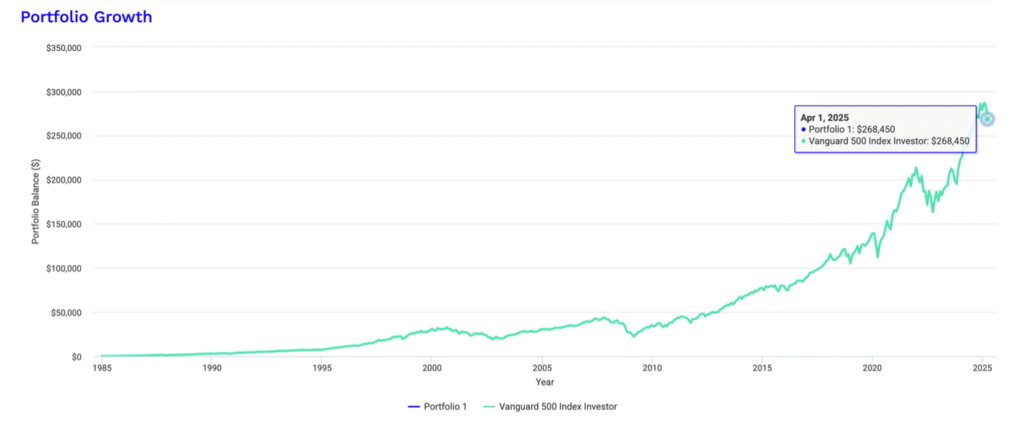

Now, imagine if I had taken the money from just one coffee per day, every day since I was two years old, indexed to inflation, and invested it in the S&P 500. I would have started with one dollar per day in 1985 and ended at about $2.62 per day in 2025, investing faithfully through severe market drops like 1987’s Black Monday, the Dot Com crash from 2000 to 2002, the Great Financial Crisis from 2008-09 and through Covid. By the time I was 42 years old, I would have an extra, wait for it…$268,450 in today’s dollars (see figure 2)! The amazing thing is that I would have only invested a maximum of $40,000 over the years. But by starting early and investing consistently through market ups and downs, over $200,000 would have been “free money” from capital gains and re-invested dividends. Money that was made passively over my lifetime, thanks to the power of compounding, while I enjoyed a caffeine-free existence.

If I could do it all over again, would I go back in time and give up every single creamy cup of java? Maybe, maybe not. Coffee has brought me a lot of joy and energy! But if giving up just one cup of coffee per day and investing the difference can potentially buy you a future of financial freedom, imagine what giving up larger expenses could do?

Repeatable steps I took that you can too!

- Download a budgeting app to your phone.

- Log your income, expenses and money you plan to invest.

- Review your budget. Is there anything you can easily cut? Anything you can’t live without? Remember that growing your wealth takes time. It’s a marathon, not a sprint, and you want to set yourself up for success by keeping the things that make you happy.

- Get to know compound interest. Download a compound interest calculator like Loan Calculator and plug a few numbers in. What would happen if you invest an extra $100 per month at 6 percent return over 5 years? 10 years? What if you invest $200 per month instead? Once you see how compound interest can work in your favor, you’ll understand why it truly is the eighth wonder of the world!

- Review any workplace pension plan or share program. Employers will often match your contributions up to a certain percentage. Consider opting into the maximum contribution if your monthly budget can handle it.

Leave a Reply