Since I first read Millionaire Teacher, I have learned more about the stock market’s incredible wealth-building power and how low-cost index funds can enable us to harness that power for our own portfolios. I have also learned more about how high-fee, actively managed funds can just as easily rob us of our hard-earned money and jeopardize our future financial freedom. This has led me to do my own analysis on portfoliovisualizer.com to see the numbers for myself.

While we can’t predict future stock market returns, we can look at historical stock market returns to see how much our portfolio would have grown over the years if we had been invested in a low-cost S&P 500 index fund for the last couple of decades. We can also see how much money we would have lost to a high-fee, actively managed fund and compare the two portfolios. So let’s get on our rhinestone-studded jump suits and disco-dance our way back to the 1970’s…

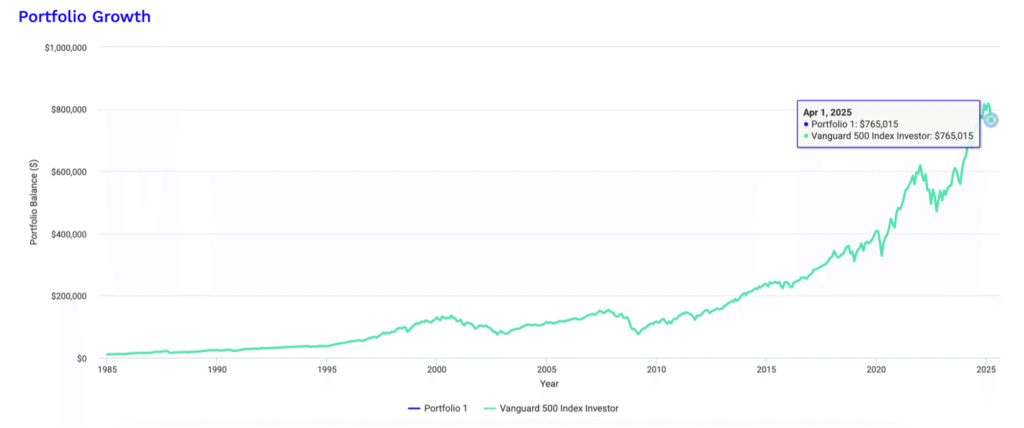

Back in 1976 Vanguard founder John C. Bogle launched the very first low-fee S&P 500 index fund called the Vanguard 500 Index Fund (VFIAX). This was great news for investors because it meant that groovy cats like you and me could finally invest in a fund that tracked the overall stock market for the low cost of 0.04%. Bogle’s S&P 500 index fund really started to take off in 1982 at the dawn of a new bull market, allowing boom-box carrying 80’s investors to invest in the stock market for a low cost. And what a prosperous investment it would have been! If we look at VFIAX’s performance through the website Portfoliovisualizer.com, we can see that just $10,000 invested in VFIAX in 1985 and left to compound over 40 years would be a whopping $765,015 in today’s dollars, even after paying the small 0.04 percent Management Expense Ratio (MER) (see figure 1).

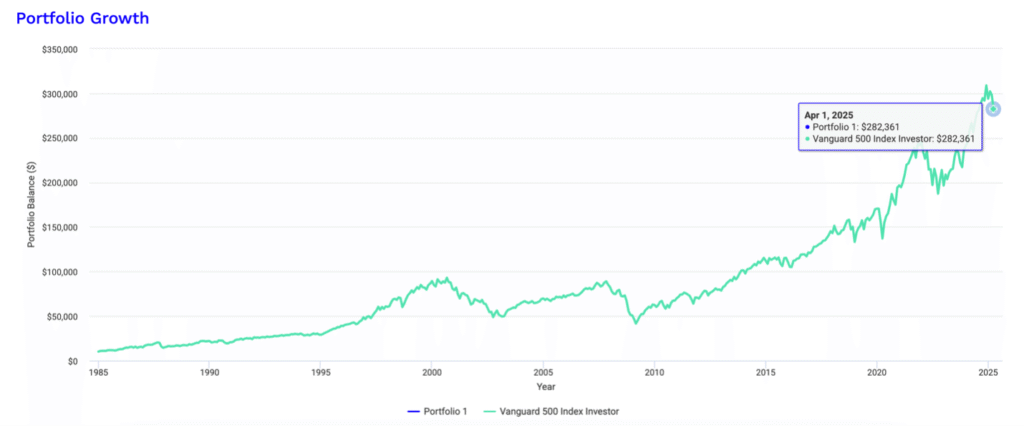

Now imagine if, instead of investing $10,000 in a low-cost index fund we had invested our hard-earned $10,000 in a high-fee actively managed mutual fund that invested in the exact same companies, but charged us a 2.5 percent MER. Surely paying 2.5 percent per year in fees would not make that much of a dent to our future wealth, right? Well, the results are staggering. Instead of having $765,015 after 40 years, we would be left with just $282,361. By paying the mutual fund company 2.5 percent every year, particularly in years when the markets were down, we would have lost $482,654 to fees! Now we wouldn’t have actually paid $482,654 in fees, but because the mutual fund company would have continued to charge us 2.5 percent during severe market drops, like during 1987’s Black Monday, the 2000-2002 Dot Com crash and the 2008 Great Financial Crisis, that 2.5 percent annual fee would have removed 30 to 50 percent more shares from our portfolio during market drops, eroding our future wealth.

Now, in theory it might make sense to pay higher fees if active fund managers could deliver stellar returns year after year, but research shows this is next to impossible. In fact, legendary investor Warren Buffet once famously bet a group of highly-paid hedge fund managers one million dollars that he could beat their actively-managed expensive hedge funds with his simple low-cost S&P 500 Vanguard index fund over a nine year period. The hedge fund managers thought they had this in the bag. After all, they had access to world-class information, a team of eager interns and the best and brightest minds in money management! But alas their victory was not to be. While the hedge funds managed to outperform the market index in the first and eighth year of the competition, Buffet’s simple but mighty low-cost S&P 500 index fund beat the hedge fund managers in seven out of nine years, winning him the bet by an average of almost 5% per year. Buffet walked away with $854,000 compared to the hedge fund managers’ measly $220,000 and a million-dollar winning prize, which he generously donated to charity.

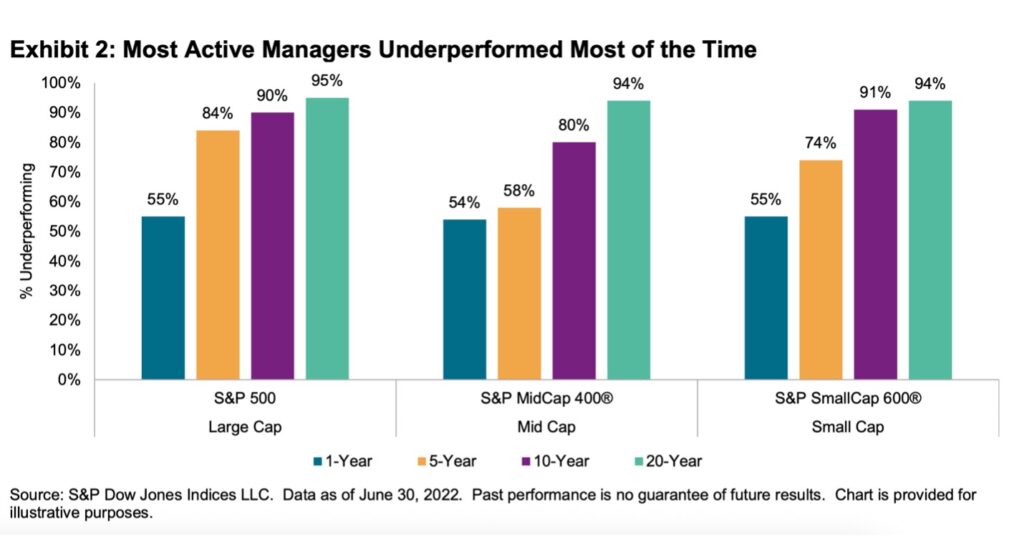

Since Buffet’s winning bet, further research has shown that active fund managers rarely beat the market index. A 2022 study by the Dow Jones Market Indices found that not only do most active fund managers underperform the market index most of the time, but they are even more likely to underperform the longer they are invested. Over a 20-year investing time horizon, active fund managers underperformed the S&P 500 market index 95% of the time, even before charging their wealth-eroding fees. Some readers of the study might argue, wait a minute, weren’t there at least some years when the active fund managers outperformed the index? And didn’t the hedge fund managers in Warren Buffet’s wager win at least two out of nine rounds, hmm? Well, the study says these occasional winnings are only due to “random luck”, the kind you’re likely to find at any given casino.

Have you ever been to a casino? I remember the first time I sat down at a slot machine in Niagara Falls. I can still hear the plinking video-game music and smell the coffee-stained carpet. I put a crumpled $20 bill in the slot machine, pulled the handle, and…won! Little red lights flashed, and jubilant music played as the slot machine tallied up my winnings. This is too easy, I thought as I pulled the handle again and…lost. Again, and…lost, until my original $20 and all my winnings were gone. The house had won. What gives? Turns out my inability to replicate my initial luck was due to the same statistical improbability that prevents active fund managers from outperforming the market year after year. Luck had won me my first round, but because Lady Luck is as random as she is fleeting, I was unable to replicate my success with subsequent spins. I may have gotten lucky once, but as the minutes passed and my clammy hand continued to pull the handle, my chances of losing only increased.

This is why active fund managers are more likely to underperform the market the longer they are invested. While random luck may give them the odd year of outperformance, there is an “overwhelming probability” that their luck will soon disappear, and they will underperform in the long run.

Once we see how much the stock market has grown over the years, and the damage that high MER fees would have made to our portfolios, we can make better investing decisions now for the future. Will the stock market continue its 100-year-long ascent and be exponentially higher in 40 years than it is today? No one knows for sure. Past results are of course no guarantee of future results. But my prediction is that consumers will keep buying products, companies will keep re-investing in efficiencies, those efficiencies will lead to higher earnings and the stock market will continue to rise over time – with volatility, bear markets and recessions along the way.

One thing is certain though. Whether the stock market continues to chart new heights or dips into bear market territory, if we are invested in low-cost index funds, we can expect our returns to match those of the stock market. But if we are invested in high-fee, actively managed funds we will undoubtedly be spending a portion of our future wealth on fund managers and lost opportunity.

Wouldn’t your future wealth be better spent on you?

Disclaimer: I am not a financial advisor. None of this is financial advice. I encourage you to do your own research.

Leave a Reply